Phone:

(701)814-6992

Physical address:

6296 Donnelly Plaza

Ratkeville, Bahamas.

Phone:

(701)814-6992

Physical address:

6296 Donnelly Plaza

Ratkeville, Bahamas.

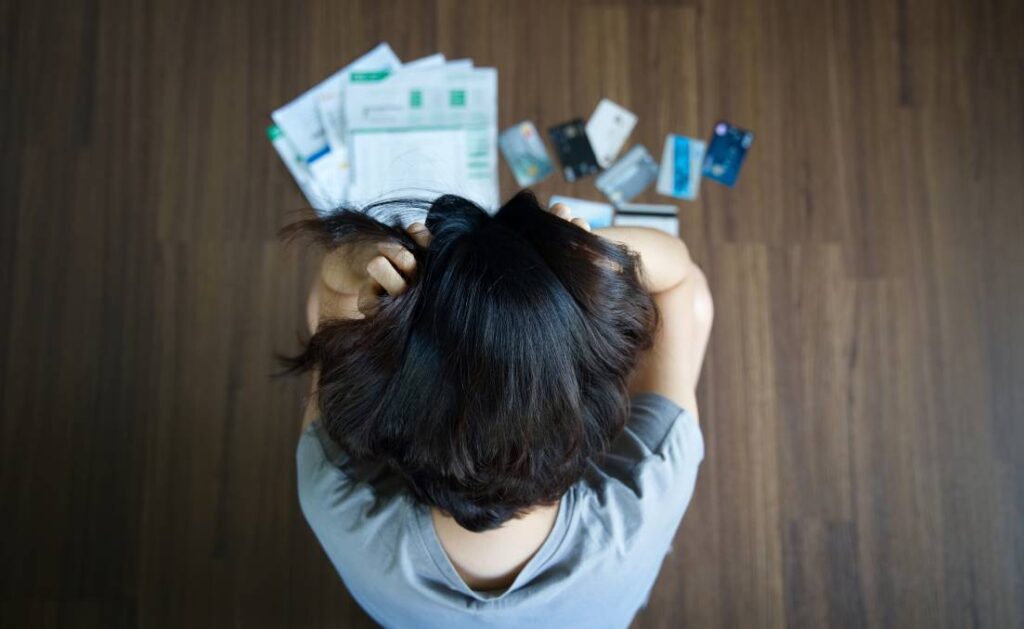

There are many things to consider when in debt. You might be scared, you can feel the pressure of you financial quagmire restraining your breathe. It is like your world is crumbling and there is absolutely nothing you can do about it. Whenever you awake, it is the first thing that fills your mind. It spoils your happiness and stretches your thought as you search for the quickest route to break free from your debts and live a life of financial freedom.

Things to consider when you are in debt:

Indeed, drowning in debt is something you shouldn’t experience; but if you are so unfortunate and you currently find yourself in this challenging situation, there is always a way out. It may surprise you to know that about 78% of Americans are living paycheck to paycheck. This simply denotes that you aren’t the only one struggling with debts.

Click here: Why You Need a Sydney Financial Advisor for Smart Investment Strategies

What should you ponder on when being submerged in debt? You should think about getting back up to the surface and one of the ways to do that is by complementing your existing income. Get a side hustle so that you can get extra cash. The extra money, coupled with your existing income should be enough to speed up the repayment process.

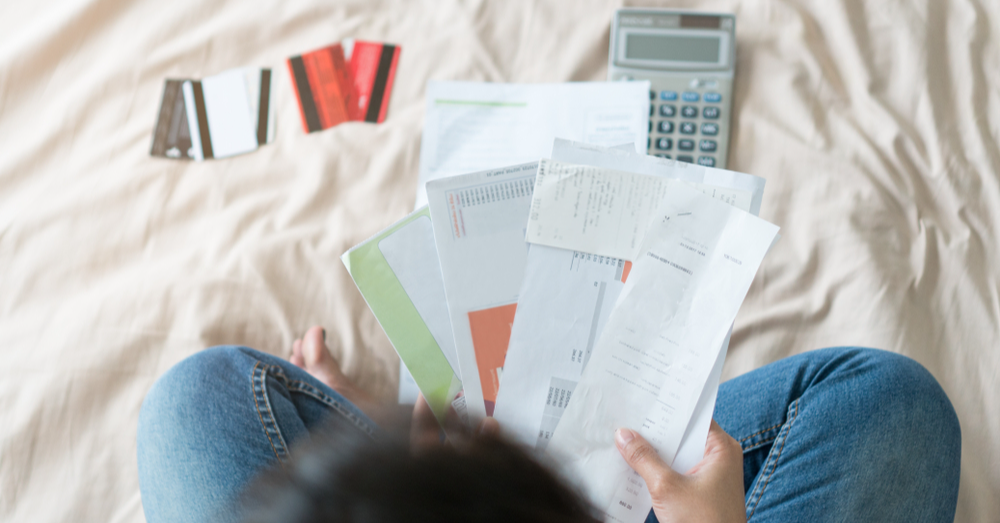

When in debt, creating a budget is one of the most important steps you can take. A budget will help you spend money on necessary commodities, it will also show you how your money is being spend. Individuals who spend wisely seldom go broke or find their self in any financial storm.

When your expenses are more than your income so many bad things happen. With a budget, the urge to draw out your credit card and make unnecessary purchases will be eliminated because you want to adhere strictly to your budget.

While creating your zero-based budget, you may feel the urge to account for your entire expenses first. The first step to take is to make sure that your basic needs are taken care of.

These basic needs are:

After you have created a budget for groceries, water, electricity, gas, rent or mortgage, you can then assign whatever is left to other urgent needs. If you have student loans or a car payment, ensure that they all go into the budget. Irrespective of how small the expenses is, still include it in the budget. Always have it in mind that if you deduct your income from your expenses, the result should be zero.

Your affinity for loans is one of the reasons why you find it hard to get out of debt. I am quite aware that this can be a very difficult decision to make, but trust me, acquiring more debt is the worst thing you can do at this period. The choice you make now, can affect not just your immediate family but your future generations. So be wise and reject the urge to take on even the smallest of debt. You can also decide to freeze your credit cards. You can either destroy it, or hide it. Yes, you may feel that having a credit card for emergency situations is a nice idea until your next “emergency” appears to be a visit to the spa. Discarding those credit cards of yours is an ideal way to put an end to the wicked cycle of debt for good.

If you are already in a huge debt and you need money, don’t take loans. There are other things to consider when you are deep in debt and in need of money.

Having created a budget, and now that you have made up your mind to stop borrowing, it is the best time to augment your income. You can either get as second job or look for a side hustle that will provide you with the extra money you need to settle your debt. The side hustle can be lawn mowing, babysitting, car washing, working at a coffee shop, etc. You definitely have to bring in more money.

I understand that you may not want to work all day, but this is one of those short-term sacrifices you will have to make to get out of debt.

Always have it in mind that you won’t be doing this for eternity. And it will help you gather more money to supplement your existing income.

Having said that, how long does it take to get out of debt? Well, this varies and it depends on several factors. But one thing I can assure you is that, if you are committed and you adopt the best tactic, you will pay off that debt of yours quickly.

Generally, we ought to be contented with what we have. We insult ourselves, unknowingly, when we compare ourselves with someone else. When getting out of debt, ensure you don’t get carried away by the extravagant lifestyle of your friend; if you do, you will lose focus, and you will also lose the opportunity to achieve the financial freedom you have always dreamt of.

When you are out of debt, you can decide to spend as you like; but remember that it is one thing to get out of debt, and it is another to prevent yourself from falling back into debt. Social media is the main culprit regarding comparison. If you observe that you find yourself always falling into the comparison trap, you can decide to take a break.

Now that you have a side hustle that is bringing in additional money, you can start settling your debts with a strategy called the debt snowball method.

If you find it hard to make payment, you can get in touch with your creditors. If you have a good credit report, and you pay your debts in time, they may be willing to reduce the interest rate or extend the time required to repay the debt. Don’t waste time, do this before your account is turned over to a collection agency. At that instance, the creditor has lost hope.

Don’t be scared to approach your creditors with the offerings mentioned above. The worst they can do is to sue you and that would cost them a huge amount of money and extra headache.

Are you struggling with lots of student loans but yet you spend like your dad is Bill Gates? Spending extravagantly can be one of the reasons why you are being submerged in the sea of debt. You have to limit how you use your credit card so you have adequate money to take care of yourself and settle your debt either by making monthly payments or weekly payments.

Cutting off unnecessary spending habits is the first step to take if you are eager to come out of debt. If you spend money on irrelevant things while in debt, you may end up regretting it – that is a fact! If need, you can remove your credit card from your wallet and keep it somewhere else so you don’t have use it unnecessarily.

While sinking in debt, you can also solicit for help from professionals. These people who are experts in getting people out of debt by offering them advices and recommendations, can help you regain your life of financial freedom.

Lots of debtors have contacted these professionals and it has worked quite well for them. You may either give them a try or you can consider going for credit counseling. Also, there are some organizations in the US that assist families financially. Contact them to find out if you qualify.

You can certainly live a debt-free life, it all boils down to you knowing what to do and taking the right steps. How do you go about this? Block or mitigate anything that would prompt you to borrow. You can do this by settling off credit card transactions pronto, saving up money, buying cheap used cars, etc.

If you are eager to stay out of debt, you have to save up money-a substantial amount. Having a large savings is one sure way to stay out of debt. Why borrow when you have money stocked in your savings account?

With your savings, you can settle your bills without any difficulty. Even when emergency situations arise, you will have no reason to borrow thanks to your savings. If you choose not to save, you will someday run out of money and you will have no choice but to borrow.

You can decide to make monthly payments into your savings account, it will eventually accumulate. Save now so you may not have to borrow tomorrow.

Many middle-class Americans find it quite difficult to make full payment when purchasing a car, so they decide to adopt a car payment. You don’t need to take a car loan. There are a variety of good used cars out there.

I am aware that there exist some risks when it comes to buying used cars, but there are also risks involved in dealing with some tricky car dealers who often upsell you on cost and limited warranties.

You can carry out an in-depth research about reliable used cars, get a good mechanic to check out the car for you, then buy based on your intuition. At the end of it all, if you are quite lucky, you may get a car that will last for a long period of time.

One way to get deeper into debt is by making mistakes people make when trying to get out of debt fast on their own. If you discover that you may need help regrading your debt, do not hesitate to contact an expert.

Renting an apartment for life seems like a bad dream for some individuals, but real estate is quite expensive. If you are eager to live a debt free life, getting a roof over your head would be a major challenge. Having said that, saving up for a good home is a good idea for most middle-class Americans (so far you don’t reside in areas like Southern California).

Of course, this could take years, depending on how much you earn per month, but spending some years renting and saving up money could eventually be a rewarding experience.